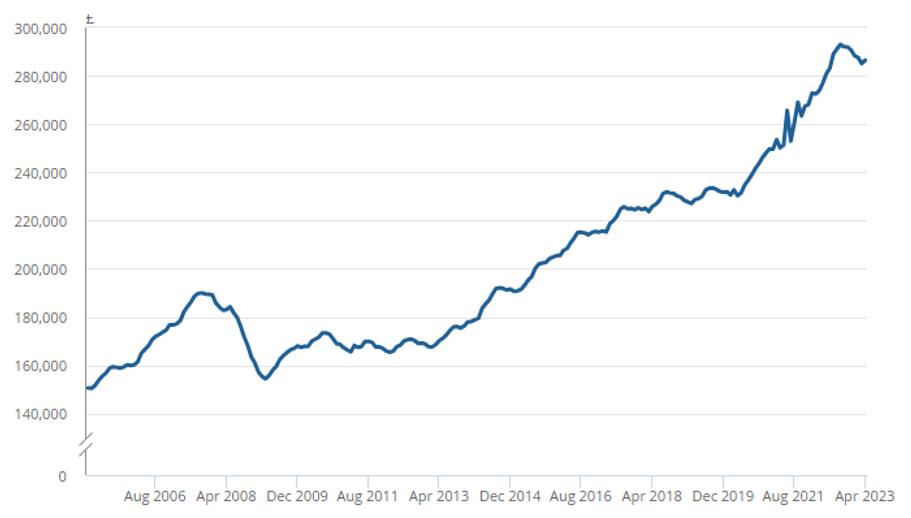

Property has long been seen as a secure and stable investment. House prices have gradually risen over time in the UK, with the chart below showing how they have changed from January 2005 to April 2023, when data was last available:

Source: Office for National Statistics

Of course, just because this has previously been the trend, past performance is not a reliable indicator of future performance, and prices may not necessarily continue to rise.

While investing in property has historically been popular, there are additional considerations you need to make compared to pursuing other assets and opportunities.

Discover four here if you’re thinking about putting your money into bricks and mortar.

1. You need to decide whether you’re investing for income or growth

Firstly, you may want to consider whether you’re targeting income by renting property out, or you’re more interested in capital growth on its value instead.

If you’re interested in income, you might focus on properties with potentially high rental yields.

One way you could inform your decision between the two strategies is by thinking about what you need based on where you are in your career.

For example, if you are early on or in the middle of your career and earning healthy wages from football, you may feel that you don’t need additional income from rent payments. In fact, all this may do is serve to increase your tax bill.

In this case, it could be sensible to invest in properties with the potential to increase in value from the start of your career to the time you think about retirement.

Meanwhile, if you’ve stopped playing professionally or are already retired, you may seek to use property to offer an alternative source of income in the form of rent payments.

Ultimately, the right option for you will entirely depend on your personal circumstances.

2. Property investments are typically illiquid

An “illiquid” asset is one that you can’t quickly sell to access the cash value in it if you need to. For example, shares in a company might be considered a fairly liquid asset, as you can typically sell them within a couple of days – depending on the particular investment and the state of the market.

However, in the case of property, it’s typically considered to be illiquid. Accessing the value tied up in a building involves complicated steps, such as employing a solicitor to carry out the conveyancing process or an estate agent to sell it – and that’s assuming you manage to find a buyer at all.

There’s nothing necessarily wrong with an investment being illiquid. In fact, in some ways, having assets that you can’t easily access can encourage you to leave them to grow over time, rather than being tempted to sell them if you need money in a pinch.

That said, before you invest, you’ll need to be confident that you can afford to have your money tied up for a potentially extended period.

3. There are various taxes you may face when investing in property

One significant consideration you need to make when investing in property is tax. There are various taxes you could face when buying and selling houses, flats, and other buildings, including:

- Stamp Duty Land Tax (SDLT) – SDLT is payable when you purchase land or property. The rate of tax you’ll face will depend on the property’s value, and there’s typically an additional 3% charge on property that isn’t your main residence.

- Income Tax – You may face Income Tax on rent payments if you let your property to tenants. The tax you could face will depend on factors such as whether you own your property personally or through a company.

- Capital Gains Tax (CGT) – You may pay CGT on gains you make on assets when you come to sell them. You do have a tax-free annual CGT exemption (£6,000 in 2023/24, falling to £3,000 in April 2024) but after that, you may have to pay tax on any increases in a property’s value when selling it. As you are likely a higher- or additional-rate taxpayer, this will be at a rate of 20%, and there’s an additional 8% charge when selling property that isn’t your main residence. That means you may face tax of up to 28% on any profits generated.

With all these taxes in mind, it may make investing in property less attractive. Make sure you prepare for them when purchasing or selling.

4. Buy-to-let rules have changed and may continue to do so

Recently, the rules surrounding buy-to-let (BTL) property have changed, meaning there are now additional elements for prospective landlords to consider.

For example, one of the major changes relates to energy performance certificate (EPC) ratings, a measure of a property’s energy efficiency.

Currently, all domestic private rental properties must have a minimum EPC rating of E.

However, all new tenancies will have to have a minimum rating of C or above by 2025. Then, in 2028, this will apply to all new and existing tenancies.

Unbiased reports that the penalty for not meeting these targets will also increase from £5,000 now to £30,000 by 2025. As a result, if your property falls below the thresholds, you will need to take steps to rectify this.

Improving energy efficiency can be an expensive undertaking. It can involve aspects such as:

- Replacing an old, inefficient boiler or heating system

- Improving heat retention and insulation in roofs, walls, and windows

- Updating old appliances and electronics, from white goods to light fixtures.

This may be another factor you need to consider before investing, understanding what sort of work you may need to carry out to ensure that your properties comply with energy regulations.

Get in touch

If you need help managing your money, please do get in touch with us at ProSport.

We specialise in helping professional footballers and anyone else involved in the game to make the most of their money during their playing career and beyond.

Email enquiries@prosportwealth.co.uk or call 01204 602909 to speak to us today.

Please note

This blog is for general information only and does not constitute advice. The information is aimed at retail clients only.

The value of your investments can go down as well as up, so you may get back less than you invested. Past performance is not a reliable indicator of future performance.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loans secured on it.

The Financial Conduct Authority does not regulate buy-to-let (pure) and commercial mortgages or tax planning.

Think carefully before securing other debts against your home.